The S-Curve Comes for Everyone – Including Nuclear Energy

Written by William Bridge, Chief Technology Officer at Nucleon Energy

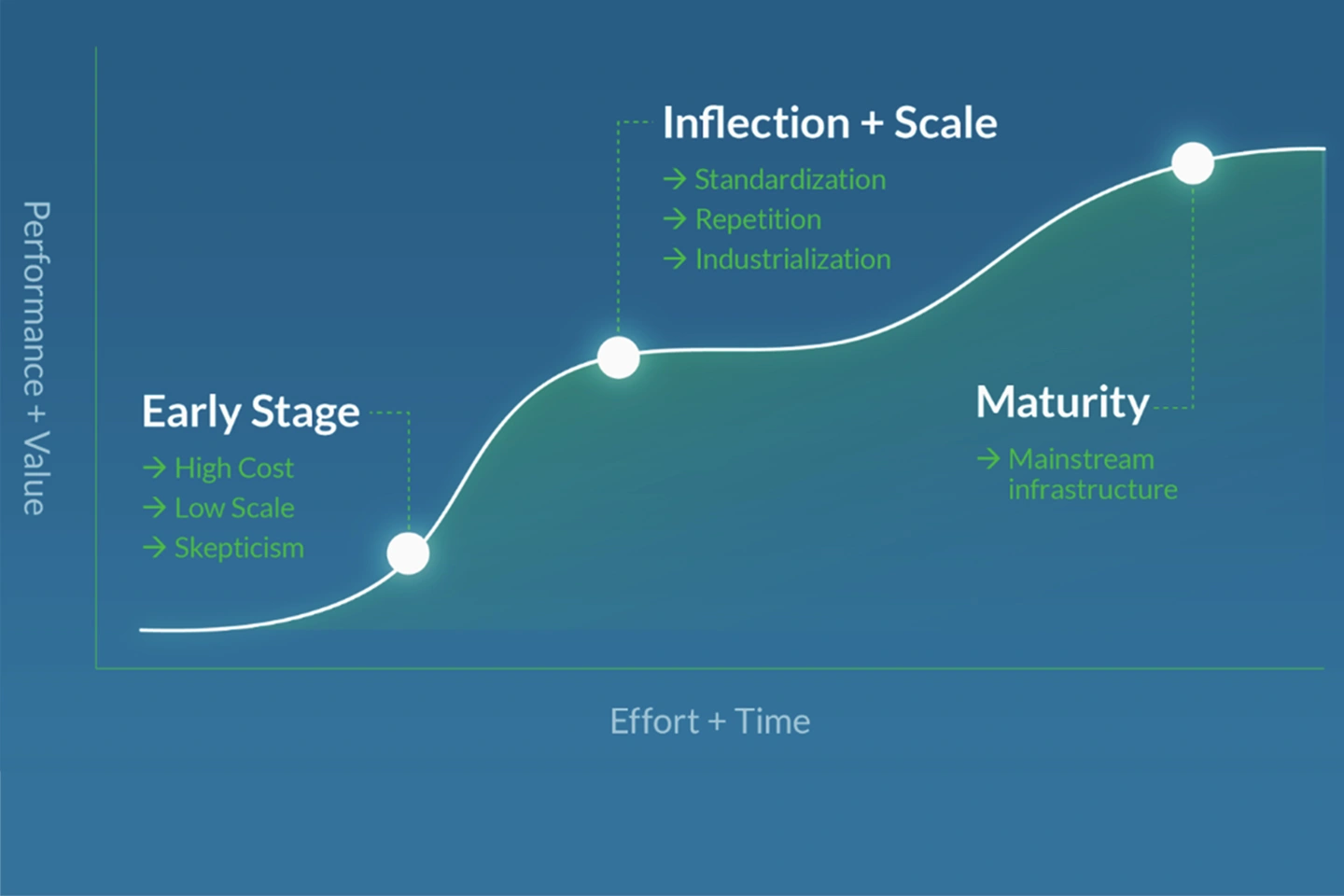

Every major energy technology follows the same arc, whether its champions realize it at the time or not. Early versions are expensive, awkward, and misunderstood. Critics point to costs and declare the whole idea impractical.

Then, something quietly but decisively changes. Scale arrives, learning compounds, and costs fall. Performance improves. The technology moves onto the steep part of the S-curve—and suddenly yesterday’s impossibility becomes today’s obvious choice.

Coal did this first. Early coal power was dirty, inefficient, and localized. Standardized boilers, rail logistics, and scale turned it into the backbone of industrial civilization. Natural gas followed. Early gas plants were niche and costly, but combined-cycle turbines and global LNG infrastructure made gas cheap, flexible, and wildly profitable. Wind and solar repeated the pattern more recently. Both were once dismissed as boutique solutions that would never compete with “real” baseload power.

The historical record is blunt about how wrong that skepticism was.

In the early 2000s, solar photovoltaic (PV) technology was widely regarded as expensive and still in the early stages of deployment, often relying on policy support and incentives to grow beyond niche markets. At that time, wholesale module prices hovered around $3.50–$4.00 per watt—far higher than typical fossil fuel generation costs and grid parity thresholds and installations were often supported by subsidies to make projects financially viable. Analysts and industry observers regularly noted that PV remained much more costly than conventional generation and that large-scale deployment depended on continued cost declines and supportive policy frameworks. Between 1981 and 2000, global solar capacity expanded relatively slowly and while growth was significant, it did not resemble the explosive scale-ups seen after 2010.

Once manufacturing scaled, global capacity multiplied rapidly and module prices collapsed—falling roughly 90% between 2010 and 2023 as cumulative production increased, supply chains matured, and learning effects kicked in. Today, utility-scale solar PV often produces some of the lowest-cost electricity in the world, a shift driven not by a change in physics, but by economics and industrialization following a classic S-curve.

Small Modular Reactors (SMRs) are now sitting at the same inflection point solar occupied in the early 2000s.

For decades, nuclear energy lived on the wrong side of the curve. Custom-built gigawatt plants, site-specific engineering, long construction timelines, and regulatory uncertainty created a cost structure that punished capital and rewarded delay. Traditional nuclear never benefited from repetition or true industrialization. Each plant was effectively a bespoke megaproject.

SMRs invert that model.

They are smaller, standardized, factory-manufactured, and designed for repeat deployment. That matters more than any single technical feature. Cost declines do not come primarily from clever physics. They come from doing the same thing over and over again, learning each time, and spreading fixed costs across volume. This is the same mechanism that transformed gas turbines, wind towers, and solar modules from novelties into infrastructure.

The early SMR projects are expensive for the same reason early solar was expensive: first-of-a-kind engineering, immature supply chains, conservative financing, and regulatory processes designed for a different era. None of those are permanent conditions. All of them improve with deployment.

Once production shifts from construction sites to factories, once regulators license designs rather than one-off plants, and once operators can point to fleets instead of prototypes, the curve steepens. Then, capital costs fall, build times compress, risk premiums shrink, and returns improve.

This is why the question is no longer whether SMRs will become cost-effective, but when they cross the threshold that solar crossed a decade ago—when the debate quietly ends because the numbers speak for themselves.

History is unkind to people who declare that a technology “will never be economic.” Those statements age poorly because they mistake a moment on the curve for the destination. Energy transitions are not ideological arguments; they are industrial processes governed by scale, learning, and time.

SMRs are not exempt from that logic. They are finally aligned with it.

The S-curve comes for everyone. Nuclear included.